On the 50th Golden Jubilee celebration of IPPTA, leaders of the industry got together to discuss the certain subjects pertaining to theme of the seminar. Each one presented his views and shared their rich experience which resulted in intellectual stimulation for all the delegates. The eminent guest gave a wonderful start at the inaugural of the seminar by providing update on the current trends in the Indian as well as global paper industry. Moving on the panel discussion carried on by industry stalwarts who provide a much needed impetus to the industry professionals to go ahead and unleash the potential and the capabilities of the Indian paper industry.

On the 50th Golden Jubilee celebration of IPPTA, leaders of the industry got together to discuss the certain subjects pertaining to theme of the seminar. Each one presented his views and shared their rich experience which resulted in intellectual stimulation for all the delegates. The eminent guest gave a wonderful start at the inaugural of the seminar by providing update on the current trends in the Indian as well as global paper industry. Moving on the panel discussion carried on by industry stalwarts who provide a much needed impetus to the industry professionals to go ahead and unleash the potential and the capabilities of the Indian paper industry.

Presented below are the edited views:-

Mr. Neehar Aggarwal, COO, Ballarpur International Graphic Paper Holdings B.V.

Congratulating the guests and the audience on the 50th Golden Jubilee of IPPTA he said “that IPPTA was formed in the year 1964 with the objective of providing a common platform to the paper industry professionals for sharing best practices, technological innovations and new developments in the pulp and paper making. It is very hearting to know that from the body of just 10 members it has grown to more than 2000 professionals till date. During the past 50 years the Association has conducted 50 annual seminars, 60 zonal seminars and 70 workshops in its quest for knowledge sharing and dissemination. To celebrate this occasion we have planned this seminar in such a way, fully befitting the occasion. With the attendee list of more than 500 professionals it is by far the biggest seminar for paper industry in India.

“The last 5 decades of the Indian paper industry has been the period of growth and transformation. The industry has taken giant leap forward and transformed itself from technological obsolescence to competitive sustenance through cutting edge technology, innovation and customer service. During these years we have seen the scale of mills go manifolds, paper machine deckle and speeds are touching new heights. New manufacturing technologies such as continuous digesters’, screw presses, dilution head boxes, shoe presses are all getting incorporated. The focus on environment and sustainability has gone up, like never before resulting in reduced water consumptions and emissions standards at par with global benchmark. As far as global paper industry is concerned we are now witnessing a structural shift in the global pulp and paper consumption pattern. The gravity is strongly in favor of Asia, India in particular. Going forward demand in India is projected to be doubled in next 10 years. In fact India is likely to contribute 20 percent to the global growth of paper demand. It means that we are heading toward very interesting times. However at the same time we are being confronted with some strong tailwinds which need to be encountered in order to move ahead. Some of the major challenges facing the industry today are price of raw material, availability of raw material, ever escalating energy prices and high cost of funds hindering the ability of the industry to expand.”

Mr. Sanjay K. Singh, Divisional Chief Executive, ITC Limited (PSPD)

Addressing the august gathering with his presidential speech he said, “I use this forum to clarify certain doubts about the paper industry. We all as a part of this industry know it all but we are unable to market our industry in a positive sense. Look at our raw material base it is trees, waste paper and agro waste, all of them can be regenerated. With this I can say that we are the most sustainable industry in the world amongst all other industry sectors. Industries like steel get their raw material from mines, plastics from oil wells and these sources will exhaust in near future. But paper Industry will continue to get its raw material from trees. So, more paper we use, more trees will be planted by the paper industry and more greener this world will become.

“Now coming on to the agricultural waste, few years back in states like Punjab the wheat straw was burnt due to which there used to be smog. Today, with innovative ideas, that whole waste is now taken in and turned into paper. The farmers are making good money and country is becoming less polluting. Likewise earlier all the waste paper was thrown into earth pitfall and allows deterioration and polluting the surroundings. This waste paper is now being used by the industry and turned into good quality paper and boards. The paper industry uses all the waste that harms the mother earth and convert it into finest of the products.

“Paper industry is known to be energy guzzlers – it is true to some extent. Compared to last 30 years the consumptions have been brought down by 25-30 percent. Let us also look at the source of energy. An integrated paper mill in India generates 50-60 percent of its energy from the black liquor that is generated during the pulp mill process. In west people are also firing the bark that is debarked from the wood into the boilers and 15-20 percent energy is generated from that. In India this process has also been started and now 70-80 percent of the energy can be regenerated form the waste. Hardly, 15-20 percent is left that we need to buy from the state grid. Today wind and solar energy has also come up. Therefore it won’t be too long that in the coming 30-40 years the paper industry in India will become self sufficient in energy by 80-90 percent.

“Coming on to water, we used be water guzzlers wherein 200 to 300 cubic meter of water was used to produce per ton of paper earlier. Today in some mill the volume has been brought down to 25 to 30 cubic meters per ton of paper. And, in the next 10 years this figure will come down to less than 20 cubic meters.

“Another concern is that we mills generate lot of solid waste. But now we have found the answer to that also. The ash generated is being used in the cement plant for brick making. Today a good paper mill in India has practically became a zero discharge mill. I have a firm belief that in the next 50 years we all will see a sea change in the thinking and attitude of the people for the paper industry.

Young people do not want to join the paper mill as all our facilities are in remote areas. Therefore it is our responsibility of market our industry in a positive sense so that new minds can be brought in.”

.

Ms. Teresa Presas, Director General, Confederation of European Paper Industries (CEPI)

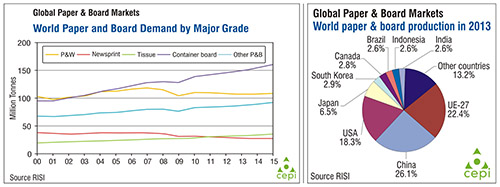

Highlighting the global trends in the global pulp and paper industry and especially in Europe she said “World demand is nearly stagnant from past 3 years (1 percent) annually since 2010 due to poor global economic performance. Demand is however, expected to improve this year and next year due to better general economic conditions. The capacity expansion is outpacing the demand growth despite shutdown in developing countries namely in Europe. The investments in China are shifting to tissue and board. Producers are having a hard time to adjust to the slower demand. An overall paper usage is lagging in the general economy.

China has it has surpassed USA and Europe in paper production and India is the growing player in this sphere.

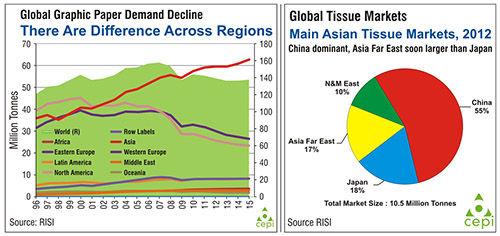

The global graphic paper sector is troubled with over capacity both with structural and increase competition from electronic media. Growth rate slowed down lately and will continue this year 2% instead of 5-7% in 2010-2011. Newsprint growth is flat. But there are differences across the region where Asia is growing in this segment.

If we turn to global packaging and board grade markets after a long twist and turn with GDP, demand has slightly under performed than GDP. GDP between years 2002-12 was 3.7 percent while the demand of packaging and board grade was slightly below 3.6 percent. Carton board market remains mature in developed countries while most demand comes from developing regions. There is big emerging growth in tissue market and China is the main driver for that.

The outlook of demand growth is prosperous but the investment plans are twice as high which means that there is a big risk of the global over capacity which is not likely to change for the next couple of years. With not so much bright outlook what is the future of the global paper industry? In this scenario innovation becomes the game changer for the industry which means best use of the resources we have.

To seize these opportunities, companies must be ready to radically reassess how they function. Many new developments are already being shaping up in some companies and research institutes. In USA the Agenda 2020 technology alliances has research and development as its priorities. The priorities are being using advanced pulping chemicals, having less water to paper dryers and introduction of new cellulose materials. These things are realistically enablers for new product development. In Canada FP Innovation is the company partnering with the industry they have the Bio-pathways Partnership Network that enables its members to explore new business ventures, develop strategic alliances, and maximize opportunities in the growing bio-economy. Japan is also looking forward to new ventures to develop new bio products ethanol and cellulose nanofiber (CNF) from wood biomass. They have also developed transparent paper into sheet forms to use for various applications. China is rather focusing on their existing assets and working towards sustainability. Brazil is not much about paper rather in raw material they have invested heavily in genetically modified trees yield in forest. Even South Africa is looking forward to bio products and trying to address their major issue which is water. In Europe the CEPI roadmap toward the carbon low economy launched 2 years ago set the vision of central role for the forest fibre sector in the bio economy. We have set goals to achieve 80% reduction in carbon and 50 percent more value with new products by 2050. The breakthrough in technology is just two paper machines or two boilers away but to be on time it should be available today. Remember the earlier breakthrough technology came 2 decades ago in the form of shoe press so we must start now.”

Mr. C.M. Vasudev, Chairman, HDFC Bank Ltd and Former Finance Secretary, Government of India

“I will discuss the issues pertaining to our economy, constraints to growth and issues that cut across many sectors and will impact the paper industry as well. I would like to start with the major things that impact us all which are economic reforms. They are basically for removing impediments to growth. Different countries endowed with similar resources have different economic reforms. Countries like China, India, Brazil and all developing nations have started at the same level but due to their different economic reforms their outlook is much different from ours. India’s growth story is also grappling with attempts in removing the impediments of growth. Year 1991 stand a much importance gear shifts where we from a centralized public dominated economy turned to the relatively open market economy which is private sector led growth economy. It is a long history of challenges and opportunities. It was a change from a self reliance to a self sufficient economy. All the development that has happened post 1991 are due to the unleashing energy and the potential of the private sector. But government has failed in marketing the benefits of the strategic reforms that were followed with which people can relate too. This is the very strong lesson that the government should learn. I hope that this is passing phase for our country and we all will once again return to the path of open market economy. Dwelling on to the some of the key issues, infrastructure development is going to be the key for our economic growth. As estimated investment of more than UDS 500 billion is needed in the next 5 years for this. Another key challenge is maintain the macroeconomic fundamentals like exchange rates, deficits etc. The biggest challenge of all is the growth of the manufacturing sector. The country of our size with the vast population to be served, this sector has to outperform all other sectors.”

.

Mr. Pradeep Dhobale, Executive Director, ITC Ltd

Sticking to the theme of the seminar Mr. Dhobale highlighted “I believe that Indian paper industry has some unique capabilities and first and foremost is our ability to use the different type of raw materials like hardwood, agro and waste paper. This capability gives us the edge to meet the paper demand of the country. Second is our ability to absorb the technology. The industry has developed the in-house technical capabilities where the paper is being churned out, given the different raw material base we use. And these technologies were not available worldwide. We developed them in-house and succeeded to a great extent. Third is the stable leadership we almost meet same people in the most of the industry events and this show our commitment to the Indian paper industry. Few days back I saw a report that Mondi reports 22 percent growth in paper profit it was something like 400 million euros i.e. 5700 crores and many of our companies doesn’t have the turnover of this size. So, when does Indian paper industry will have this kind of growth? This is the question we have to address.

Stressing of the solutions of the constraints he said “our ability to deal with the government should go multifold. The strategy should be such that we should present ourselves as a part of the solution rather than simply asking for the benefits related to tax, water, power etc. For instance if offer to be a part of their support mechanism for food security and along with that we do our pulp wood plantation we can expect different reaction. And, seeing the long term scenario of 20-25 years we have to crack this and communicate effectively. Another problem that industry is facing is the talent acquisition and in this we also have to become the part of solution.”

.

Mr. R.R Vederah, Managing Director and Executive Vice Chairman of Ballarpur Industries Limited (BILT)

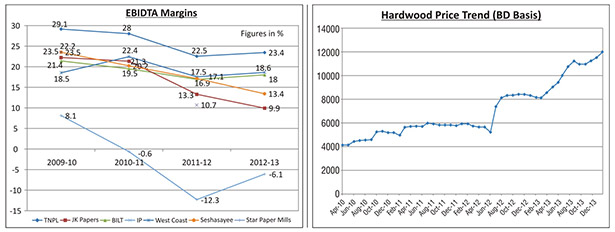

From 2007 onwards BILT has invested Rs. 6000 crores of capital in the paper business which means that we believe in the business and its sustainability. We would have easily doubled our capacity to a million ton but, the company got stressed. As we didn’t anticipate the time to achieve our objectives we have set before we went for investments. Our major investments got in taking over Sabah forest where we doubled our pulp capacity. Then in India we went into two major organic developments wherein we set up 1 paper machine and a very large pulp mill at Ballarpur unit and a paper machine in Bhigwan unit. There was a time when Ballarpur used to get 25-30 percent EBITDA on a standalone basis. But as per the statistics today many mills are running at the margins which are not sustainable at this level. The cost of borrowings places an added pressure which hammers our margins brutally. As compared to the international companies 15% margins is believed to be good because their cost of funding is zero.

The positive thing is that we have the lot of headroom to grow as compared to world average demand of 55 kg. The concerned area is GDP that contracted less than half, which we didn’t expect when we did these investments. The expected time to reach 20 million tons by 2020 from the current 13 million tons will take a little longer. During the span of 20-22 months the prices of raw material has increased by 120 percent. Today this cost of raw material for producing a ton of paper is by far the costliest in world. Getting a healthy bottom line with this kind of cost is very challenging.

But good things have also happened. Due to the increase in prices of raw material the plantation activities in the country has increased. All of us who have invested in the higher technologies have actually addressed the environment issues but with the emergence of new regulations every now and then, the stress is always there. We have the ability to absorb technology and the time has come where we have to invest in technology and R&D and find certain breakthroughs for ourselves. Likewise at BILT we are trying to increase the plantation yield by 10% and if we achieve the half of it then it will be a great compressor to the increasing raw material cost.

.

Mr. W Michael Amick Jr, President, IP India and Executive Chairman, International Paper APPM Ltd

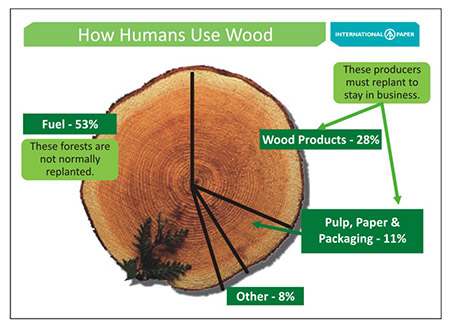

Whosoever says that paper industry is not sustainable… its “wrong”. We have planted more trees then what we cut. Pulp and paper industry is one such industry that put forward some of the best practices for sustainability which enables to manage the forest sustainably and help to increase the green cover. We as leaders must stand up and tell the truth. On the worldwide basis 10 percent forest is what the pulp and paper uses out of the total availability. On the contrary the other industries that are in the business of wood products use the forest to the extent of 28 percent. Last year on October 2012 IP APPM has planted its billionth tree and I am sure we didn’t used the billion trees for ourselves. Amick’s has 3 generations of working in International Paper and I strongly tell my son to work for this industry as it is a very viable and a sustainable industry.

.

Mr. Rahul Khanna, Director, Khanna Paper Mills Ltd

The need of the hour is that the leaders of the industry should come together and add some value to the industry over and above their individual interests. The people always perceive paper industry as a polluting industry because we haven’t taken any concrete steps till date to washout this wrong perception. We have to do something or else we are going to face bigger issues related to our image in the coming years. Another problem, that is growing bigger and bigger with the passing time is availability of the skilled manpower. There also the industry leaders have a very important role to play. Collectively we have to strategies and develop resources to generate more people for paper industry going forward. We also have the greater responsibility to improve our efficiencies in our respective companies and this pertains to the smallest of the paper mill which are contributing to the industry.

.

Mr. Rajinder Gupta, Chairman, Trident Group

The only solution left with the companies is to reinvent themselves in relation to the external environment. It will somehow help us to adapt to the situations and side by side some alternatives have to be searched for. We have to be lean which means less waste and less waste means using fewer resources. Companies have to become more open to ideas and solutions from external parties. How to add value in every process is what should be our focus. I would say that economic environment is what drives our decisions on efficiencies and sustainability. Therefore a suitable action plan has to be devised where the interest of our shareholders is safe also the required efficiencies can be achieved.