The Indian paper industry has enjoyed rising revenues and profits in recent years. However, these gains have not been evenly shared among the top players. A new study by Kanvic Consulting finds Indian paper companies must act now to transform themselves to overcome the growing challenges of increasing imports, rising commodity prices, and intensifying digital disruptions.

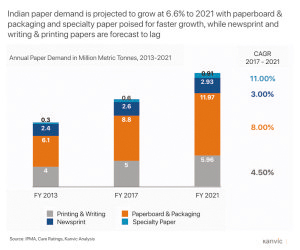

An air of optimism has surrounded the Indian paper industry in recent years as the industry has continued to grow, with domestic demand rising from 12.8 million metric tons (MMT) in 2013 to 17 MMT in 2017 at a CAGR of 7.35%. All major paper product segments have seen growth over this period, with particularly impressive performance in paperboard & packaging and speciality papers. This has also been reflected in the revenues and net profit of leading companies, which have grown at a CAGR of 4.2% and 13.48% respectively. The average EBITDA margin among the top 37 paper companies now stands at 17.76%, up from 14.2% in FY 2015.

Rising demand for paper can be attributed to a number of key factors. Across the board, rising disposable income is increasing both direct and indirect paper demand. In line with this, the country’s rising literacy rate has increased demand for books and textbooks. In addition, India’s booming e-commerce and retail sectors have accelerated consumption of paperboard & packaging, whilst growing concerns about plastic packaging and the recent plastics ban in Maharashtra has resulted in a transition to paper-based alternatives. Furthermore, premiumisation is driving industry growth as consumer product companies seek to differentiate themselves through higher quality packaging, requiring more premium papers.

Rising demand for paper can be attributed to a number of key factors. Across the board, rising disposable income is increasing both direct and indirect paper demand. In line with this, the country’s rising literacy rate has increased demand for books and textbooks. In addition, India’s booming e-commerce and retail sectors have accelerated consumption of paperboard & packaging, whilst growing concerns about plastic packaging and the recent plastics ban in Maharashtra has resulted in a transition to paper-based alternatives. Furthermore, premiumisation is driving industry growth as consumer product companies seek to differentiate themselves through higher quality packaging, requiring more premium papers.

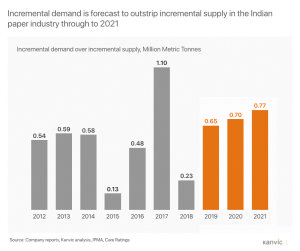

While demand has been steadily increasing, favourable conditions have been further improved by the falling prices of the key input – waste paper. Since China imposed a ban on the importation of waste paper in 2017, the global price has fallen over 6%. Indian paper companies have further benefited from the tight supply scenario as incremental demand has outstripped incremental supply in each of the past seven years and the gap is forecast to increase further through to 2021. As a result, the industry’s capacity utilisation rate has increased and now stands at 86%

Winnings, Not Evenly Shared

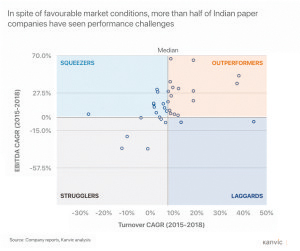

Despite favourable conditions in the paper industry, gains have not been shared evenly. New analysis of the performance of top Indian paper companies since 2015 by Kanvic Consulting has identified four distinct performance-based groups.

Despite favourable conditions in the paper industry, gains have not been shared evenly. New analysis of the performance of top Indian paper companies since 2015 by Kanvic Consulting has identified four distinct performance-based groups.

Fewer than half (46%)of paper companies are classified as Outperformers, growing their revenues at above the industry median as well as improving profitability. While 31% of companies are classified as Squeezers, growing below the industry median but still increasing profitability. However, 17% of paper companies are Strugglers who have grown below the industry median and also seen their profitability decline. Lastly, the remaining 6% of companies are Laggards who have had above median revenue growth but watched their profits fall.

This analysis shows a clear need for the majority of Indian paper companies to improve performance to realise the benefits from the favourable market scenario. Furthermore, with new challenges looming for the Indian paper industry, even past Outperformers will need to revisit their strategies to ensure future success.

Looming Challenges

Although growth still remains robust for Indian paper companies, the Kanvic report finds that the industry faces three key challenges.

Firstly, imports pose a growing threat to the competitiveness of Indian paper producers as they are growing at a faster rate than domestic demand. This has been driven by imports from large integrated paper mills in the ASEAN region operating at greater economies of scale. In addition, these companies have benefited from a Free Trade Agreement signed in 2014 removing most import duties. While the Indian paper industry continues to lobby for change regarding the duty structure, it seems likely that Indian players will have to contend with the rising threat of imports for some time.

Secondly, the steady rise in commodity prices is increasing production costs for Indian paper mills who generally rely on captive thermal power plants. This is significant as energy costs typically account for 13% of Indian paper mills cost compared to only 8% for international players. The recently imposed ban on the use of pet coke as a fuel will also increase costs for many players. Furthermore, rising oil prices also increase the already high transportation costs for paper.

Secondly, the steady rise in commodity prices is increasing production costs for Indian paper mills who generally rely on captive thermal power plants. This is significant as energy costs typically account for 13% of Indian paper mills cost compared to only 8% for international players. The recently imposed ban on the use of pet coke as a fuel will also increase costs for many players. Furthermore, rising oil prices also increase the already high transportation costs for paper.

The third challenge for Indian paper companies is the fast-emerging digital revolution which is poised to bring about a radical change in an industry which has been historically slow to adopt new technologies. The deployment of low-cost sensors, cyber-physical systems like robotics and cloud computing are combining to bring about major productivity gains.

As progressive paper companies adopt digital technologies they will become more agile and be able to reduce costs, putting pressure on laggards to remain competitive. Many paper industry customers such as FMCG players are at a more advanced stage of the digitalisation journey. Therefore, they increasingly demand that suppliers integrate seamlessly with their digitally enabled supply chains – accelerating the pace of digital transformation across the industry.

Finally, the Kanvic report also finds that the rise of digital is also poised to disrupt current industry boundaries. For example, they point out that leading global paper equipment manufacturer Voith recently launched merQbiz; a global marketplace for buying and selling waste paper. Such moves have the potential to displace existing intermediaries in the waste paper business as well as concentrating ownership of valuable market data.

Transform to Succeed

Through extensive experience and study of the paper industry in India and globally, Kanvic has identified 4 key areas where Indian paper mills must transform to succeed in this changing environment. These are strategic thinking, manufacturing excellence, marketing orientation and digitalisation.

Through extensive experience and study of the paper industry in India and globally, Kanvic has identified 4 key areas where Indian paper mills must transform to succeed in this changing environment. These are strategic thinking, manufacturing excellence, marketing orientation and digitalisation.

When it comes to strategy, Indian paper mills need to identify where and how to compete and optimise their product portfolio to maximise profitability. Through a disciplined focus on categories and customers where there they have a clear and sustainable competitive advantage, paper companies can build a strong value proposition and capture pricing power.

In addition to this, Indian paper companies must transform their manufacturing operations by benchmarking with the best externally, adopting lean practices and upgrading, engaging and encouraging innovation from their people.

Furthermore, Indian paper companies must bring greater marketing orientation to their business by gaining a better understanding of their real customers, developing more effective customer targeting and shedding the commodity mindset. Historically Indian paper manufacturers have been detached from their customers due to the influential role of dealers. However, as paper customers become larger and more organised, the industry structure will gradually shift. Those companies that move early to gain a deeper understanding of customer needs and build stronger relationships will gain advantage.

Finally, firms that act on the clear opportunities presented by digital will be best placed to outperform their industry peers in the next act for the Indian paper industry. There is huge scope for digitalisation, in manufacturing, logistics, procurement, marketing, and sales. For example, companies can reduce costly unscheduled downtime through real-time monitoring of machinery via IoT devices and then leverage Artificial Intelligence to give alerts on when to perform preventive maintenance.

In light of the emerging challenges and opportunities in the Indian paper industry, it is clear that companies that take concerted action to transform themselves today in strategy, manufacturing, marketing, and digital will be best placed to outperform their industry peers in the years to come.